|

Can you believe it's that time of year already. As we wind down 2017 and usher in 2018 it's time to look a head and set some New Year's resolutions. Whether you accomplished everything you set out to do in 2017 or not a new year means you get another shot. I don't know about you but I'm going after everything I want in 2018 just as I did in 2017.

Did I miss the mark on a few of my resolutions from last year? Absolutely, but I also achieved some amazing things that I would not have, if I hadn't taken the time to dream big. So here we are going into 2018 and I'm dreaming even bigger this year and I encourage you to do the same. Today's show was partly inspired by an article from www.forbes.com . 7 Keys to Keeping Your New Years Resolution in 2018

Key #1: Be Crystal Clear - When it comes to setting goals this is one area that many people need help with, including yours truly.

Key #2: Can't Measure What You Don't Track - As state above the M in S.M.A.R.T. goals stands for measurable. In the words of my mentor Brian Beane "You can't measure what you don't track!" In order to make the proper course corrections along the way to your journey, you absolutely have to track your progress. Otherwise how can you ever know if you've gotten off track are if you've already hit the mark. Too many times we resolve to do something and don't track the results. Key #3: Reaching Your Goals Requires the 5 "P's" - You're going to need a heavy dose of the 5 "P's" to keep your resolutions. Perseverance, persistence, patience, permission to fail & procrastination (stop it). You will get knocked down on your way to fulfilling you new years resolution and you're gonna have to persevere. Before you get knocked as well as after you get up there will be things that constantly pick at you, distract you and test your resolve, you have to persist and keep moving forward. While success isn't built in a day, it is built daily! You're gonna have to be patient! You want success badly, I get it, but allow your efforts to compound. As long as you're taking daily actions, you'll get there. Permission to fail is a big on that most people miss. Don't beat yourself up when you fail. No I'm not saying you'll ultimately fail at your goal but I can promise there will be little failures along the way. Give yourself permission to experience the fullness of those little setbacks so that you can learn from them and get better. It's sulking over these little failures that cause most people to quit on the bigger mission. Know that these things will happen, try to anticipate them and create contingency plans for them but above all don't be defeated by them. Finally STOP PROCRASTINATING!

Key #4: Go Public - It can be tough to deal with the ridicule of family and friends sometimes when you're trying to accomplish something. Especially if they don't believe in you or the think your goal is too big. People love to superimpose their limitations onto others and that's why they tend to have only negative things to say to and about people that aspire to greatness. They are basically saying if you even attempt to accomplish something great it will shine a light on my lack of ambition. Don't let these people play mind games with you because they don't have the mental capacity to dream big.

With that being said, you have to go public with your New Year's Resolution. You're gonna need someone to hold you accountable, someone to encourage you and yes someone to hate on you. Going public is the only way to find the right people to do all of those things for you. For the most part you won't get all of these levels of support in the same person. Yes, haters are also your supporters. Remember, haters only have one job, that's to make you better. So let even your haters know what you're goals are so you can use their hater tactics as motivation to push through. Key #5: Plan Plot & Strategize - Yet another big mistake made by Resolutionists, is that even a word lol. They never plan. In fact they treat there resolution as if failure is a foregone conclusion. Sometimes they even say them with a smirk as to say that which is being proposed is a mere fantasy and is impossible for them to accomplish. However, if you're serious about your resolution for 2018, prove it. Devise a plan to actually achieve it. That's the difference between a goal and a wish...a plan. Once you've laid out your resolution for 2018 with clarity, work backwards from them to devise a plan of action. Break the plan up into daily actionable steps that can be measured and charted. Again success isn't created in a day but it is created daily. A bunch of tiny actions with a singular focal point in mind compound over days, weeks, months and even years is how success is created. Your new years resolution for 2018 should be part of an even bigger vision & plan. As they say the path to every destination begins with a single step. Your resolution has NO validity until there is an actionable plan in place. Key #6: Make Time for It - Time management is something that I've struggled with all my life and I know I'm not alone. If you're going to keep your resolution you're going to have to make time for it. Yep, actually put your daily action steps on your calendar. One of the things that I'm implementing now is a daily "To Do List." Every night before I lay down, I gather my family for 15 minutes or so to help me put my list together. The family is important as I need to know if they have an expectations of me for the coming day and I need to write that down. By default I'm teaching them this little time management hack as well. I get everything needed down on a piece of paper then I prioritize it into my calendar for the next day. This not only helps me be more productive but it also helps me keep a running tally of my progress. For every task that doesn't get completed goes on the list for the next day. When too many tasks go unfinished from the previous day it causes me to reflect on how I spent my time and whether or not I really want to achieve a particular outcome. Key #7 - Give Someone Permission to Hold You Accountable - People say the reason they hold their goals to themselves is because they don't want anyone to steal their ideas when in truth they don't want to be held accountable. If you're going to be successful at keeping your 2018 new year's resolution, you have to give someone permission to hold you accountable. Someone other than you must know the details of your plan, the actionable steps and time frames for which you intend to accomplish your goals. It's only then can they truly hold you accountable and call you to task. I like the idea of an accountability team. Not just one person but a group of people that you'll need to answer to when you start slacking. Again, you want family members, friends and even haters to know what your goals are, as they all serve as different types of motivation and inspiration. Follow these 7 Keys and you'll be able to Keep your New Year's Resolution for 2018.

Today's show was inspired by Bustle.com - If you love to read great written content this site provides great content. Check out the specific post that inspired today's show by clicking here!

My 8 Financial Resolutions to Consider for 2018

#1 - Don't try to keep up with the proverbial Jones' - The Jones' have single handedly killed more financial legacies than any other family on earth, lol. It's extremely hard to do when every piece of advertisement we see pits us against one another. However, if you can learn to stay focused on your financial goals and NOT worry about what everyone else is doing you'll be fine.

#2 - Invest/Save Before You See It - Try automating your investments/savings. It's amazing how far we can make our last few dollars stretch. Well, guess what? We can make most of a pay check (less a set amount that goes to a savings or investment account automatically) stretch just the same. You'll actually learn to adjust rather quickly to the new take home pay amount. I once had my pay check being garnished because of student loan debt. I was pissed when I found out they were going to be taking my money, as if I didn't know I owed them, but within 2 weeks the adjustment was made and we didn't really miss it. The same is true for you, have money from your pay check directly deposited into an investment or savings vehicle automatically then adjust your budget to live off what's left. It's harder make the decision to do it than it is to actually do it. You're gonna have to trust me on this one. #3 - Get To Building Your Emergency Fund - I know you hear the financial minds say it all the time, and you agree that you need one but putting money somewhere without touching it is just easier said than done. One thing you can do is set up a savings account in a bank that's very inconvenient to get to. Maybe one that's a couple counties over and make sure you DON'T elect to receive a debit card or checks to that account. Doing this will force you to think twice about accessing that money to make impulse purchases. Chances are by the time you go through what's needed to access the funds in the remote account the impulse would have subsided.

#4 - Max Out Your Company's Match - It's FREE MONEY! I don't know how else to say it. Just like with #2 Invest/Save before you see it, whatever percentage your company is matching you, figure out a way to maximize your contribution to meet that amount. Sometimes it's a matter of scaling back just a little but it's definitely worth it. Again, it's FREE MONEY.

#5 - Get Your Credit Tight - We've all heard it said that cash is king. While that might be a true statement, credit has ruled this kingdom for a long, long time. Most working class people are just now beginning to understand that. What is credit? Basically it's your reputation in the market place. As the Bible says "a good name is more desirable than great riches." Let's face it, having bad credit is something that we literally CANNOT afford. The interest on borrowed money with poor credit vs good credit could mean the difference between living check to check and having extra money left to invest or build an emergency fund. "A good name is to be more desired than great wealth,Favor is better than silver and gold. " Prov. 22:1

#6 - Get Your Taxes Under Control - Most working Americans don't realize that taxes are their largest expense and even fewer understand the control that they have over their income tax. Yep, you heard that right, of all the many fixed taxes that we are required to pay, there is one that we actually have control over and that's our income tax. We dictate to our employer how much money to withhold from our paychecks for taxes. Depending how long you been on your job, you might not even remember completing form W4, the Federal Income Tax Withholding certificate. But you did and you told your employer exactly how much to withhold from your pay check for taxes. According to the IRS upward of 80% of working Americans completed the form incorrectly and are having TOO much money withheld from their pay. Just correcting a simple mistake could transform your finances. Last year I help a married couple increase their take home pay by $1000 per month. The wife was overpaying $700 per month, hadn't revisited her W4 since she'd been on her job even though she'd since gotten married, had 2 kids and started a business. The husband was overpay by $300 per month, so that $1,000 monthly increase transformed their finances dramatically. Getting control of your taxes can go a long way towards righting your financial ship. #7 - Read, Listen and Hang - This is probably the easiest of them all, once you get through the first couple of days. You are who you are because of 3 things primarily, the books you read, places you go and the people you associate with. It's time to increase your financial I.Q. Therefore you'll absolutely have to start reading books, magazines and blogs on the subjects of money, wealth, credit, capitalism, taxes etc. You'll need to start listening to podcast and other content regularly on the subject of money. Don't be afraid to redraw your circle either. Too many times we feel guilty about leaving old associations behind. Friends, family members even significant others that aren't focused on the same things you are at this stage in their lives may have to get left behind. It sounds harsh but how long are you willing to stunt your own growth for those that aren't willing to grow at all. Sometimes it's a matter of praying for them and moving on. An unforeseen benefit of moving on in life is the inspiration that it causes others to feel as you prepare to move forward without them. So in a sense, you stunting your own growth may very well be pacifying the complacency of those around you. Don't be afraid to be great. In the words of one of my favorite entrepreneurs and vloggers Na'Kesh D. Smith, "the sun don't give a f*ck who it blinds when it shines!" You cannot afford to dim your light for fear of intimidating someone that can't handle your greatness.

#8 - Start Your First Business - It's said that 9 out of 10 business fail. i don't know how true that is but I was so determined to become a successful entrepreneur that I was prepared to start at least 10 businesses. That's why I say make an effort to start your first business in 2018. As much as I'd like for this endeavor to be wildly successful, chances are you're going to have a rough go at this thing we call entrepreneurship. However, now's as good a time as any to start your first business.

In today's economy and with today's technology there are tons of businesses that you can start for very little out of pocket costs. Take your bumps and bruises early and often but more importantly, learn the lessons and grow. You may now be successful the first go around but you'll learn valuable lessons that will make the second time around more tolerably. Then there's the uncertainty of the job market in this economy, yet another reason to give entrepreneurship a shot. Take the recent Newsweek Article stating the proposed thousands of lay-offs from one of the big Telecom companies. Sobering news for those employees this time of year. Even if your company is doing well, in my opinion the very best time to prepare for storms is when the sky is clear and the sun is shining bright.

So you read yesterday's blog and you're thinking to yourself, "there's gotta be another way to build generational wealth without the radical sacrifice!" You're right, there are other alternative methods to building wealth but they all require radical sacrifice. You may not have to scale back your entire life to the bare bones minimum but you're going to have to give up something. It's a universal law of sowing and reaping. If you want to reap a harvest of wealth you have to sow the seeds that will produce such a harvest.

Setting the Atmosphere for Breakthrough

At the core of the Generational Wealth Blueprint is the "Catalyst." Everyone has to start somewhere and the fact that almost 80% of Americans are living paycheck to paycheck, the catalyst is the only logical place to start. "What is a catalyst?" you may be wondering. It's that one "small" thing that creates something massive. Think about a tiny acorn that produces one massive Oak tree, that produces millions of acorns that will become thousands of Oak trees. Or think about the tiny snow ball that tumbles into a massive avalanche. How about that single spark that ignites a wildfire. You my friend will need a catalyst to start the ball rolling to generational wealth. Lucky for your, if you don't want to live like a hermit for the next 10 years there are other strategies available to you.

In the examples previously describe the "Catalyst" is the one single thing that we can point to that to catastrophic events. We know however, that the "Catalyst" was just the right stimulus at the right time, the culmination of a sequence of events that was merely topped off by the catalyst. I mention that because working class people in America are in prime position for a financial catalyst to spark catastrophic change in their lives. The right catalyst can spark a positive change, but the wrong catalyst can send a person on a downward spiral into depression, despair and even death. The conditions are ripe, the stage is set for either one to happen. A lifetime of financial struggles and economic injustice. We're working harder and harder to live of less and less. Yes the stage is set, the question is..."are you ready?" Build an Asset to Buy an Asset

So we've come to the conclusion that you scaling your lifestyle back to the bare minimums is out of the question. Not that you're not passionate about building generational wealth, or like Dame Dash says "Hustling for your last name." You're just looking to sacrifice in other areas because we've also established there is no way around sacrifice. If a financial catalyst is what we need you really only have three options, spend less, earn more or a combination of the two. Since you don't want to spend less let's focus on earning more.

Everyone on this planet is an expert at something, but few are experts and turning that expertise into profits. I've been saying for years that 2 people will always be able to eat on this planet, the person that can work with their hands and the person that can sell. In this digital age we have to add a 3rd person to the list and that's the person that can teach what they know to others. With that being the case and you needing a financial catalyst ask yourself, "What can I do that others would pay me for?" Yep, you heard me right, if you need a financial catalyst, you may just need to start your own small business. Wait, don't pass out on me, I'm talking about making a couple hundred dollars per month in addition to your primary income. Hell, you can collect beer cans if you wanted to and make that every month. The question is, "are you sick and tired of your situation?" Why is starting a small business in your home such a great way to get the financial catalyst you need to start your generational wealth building game plan? It's simple, as a business owner you get to play by a different set of rules. Remember those 4 challenges that we talked about in part 1 of this series, with taxes being one of them? What if I told you that you could likely get a $200 monthly increase in your household cash flow just by registering and starting your business from home regardless of whether or not that business makes a profit the first couple of years? Well this certainly isn't tax advise because I'm not licensed to do that, but that's exactly what I'm telling you. Every working class person in America should have a home based business in their wealth building portfolio, and here's why! Uncle Sam...Friend or Foe?

The U.S. tax code was written for business people, by business people therefore it benefits business people. Because of this truth, everyone looking to build wealth in any capacity should have a business in their portfolio. The average person that starts a small business from home will save $12k-$15k per year in taxes. Is it starting to click yet? What could you do with that tax savings or that financial catalyst? You guessed it, build an emergency fund, pay off debt or invest. So whether you're good at baking, fixing small engines, babysitting or tutoring kids on the weekend, turn it into a legit business and start saving money on your taxes. If you should happen to be good enough to make a profit, that's even better.

Let's just play around with some numbers for a second. Say you started your business from home, you're able to adjust your W4 form on your job to reflect that you're an entrepreneur which means fewer taxes will be withheld or in other words you'd give yourself a monthly pay raise of a modest $300 per month. Your business brings in an additional $200 worth of profit. Again, you can likely collect $200 worth of aluminum cans on a single weekend if you wanted to. Just like that you have a $500 monthly catalyst. If you were smart you'd take the extra $500 and start paying off debt to free up even more monthly cash flow or work on your mini emergency fund. Instead however, you keep paying your debts as you normally do and you take the $500 per month and prepare for investing right away. What could $500 per month actually become at a descent rate of return (believe it or not double digit returns are normal if you know where to look).

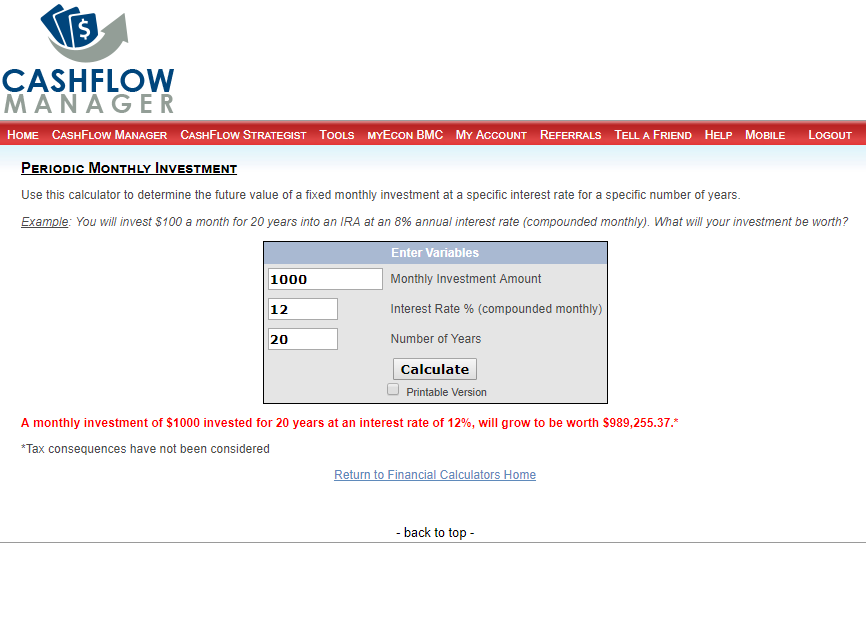

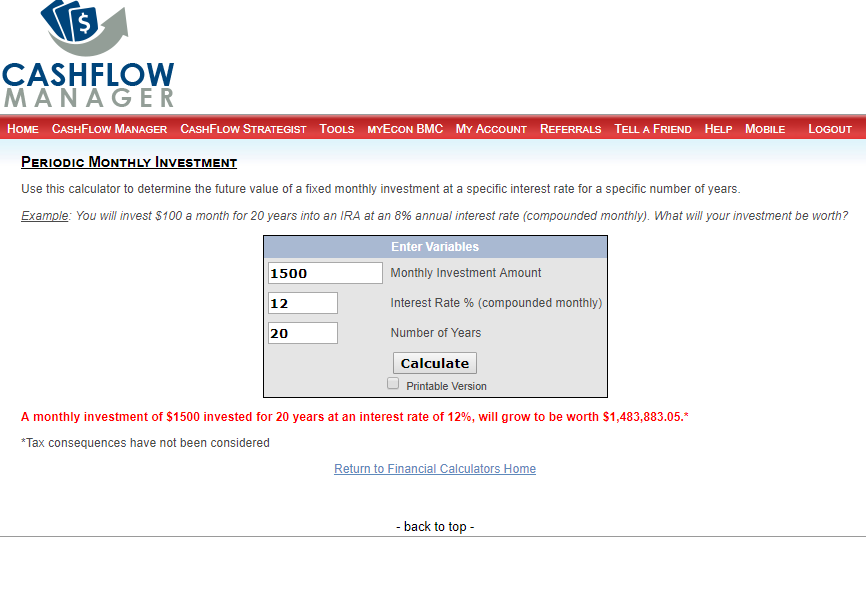

In the 3 images above you see what it looks like to build generational wealth $500, $1,000 & $1,500 at a time. Do you think it would be worth it to find a way to turn at least one of your gifts, talents or passions into a business for the purpose of multi-generational wealth creation. i believe without a shadow of doubt there, something that you can start doing right now and build a profitable business from home to the tune of $300-$500 per month. Now that you can see what will happen if you put a little more effort into it, you can likely build far more that $500 per month in additional cash flow. The key becomes, finding a way to generate the extra income passively. That's next level wealth building because you can have the best of both worlds. You have the extra cash flow to pay off debt and invest but you wouldn't have to give up all your time to get it.

There are literally millions of ways to generate passive and residual income so I won't bore you with a pitch here. I will say that sticking to things that directly involve or are closely related to something you're passionate about is the best place to start. As you can see, no matter how you slice it, building generational wealth will take sacrifice, but I think it's worth it.

Building generational wealth should be at the top of mind for every adult on the planet, in my humble opinion. Who doesn't want a better life for their children and grandchildren. Well according to the latest statistics, not many. Generation wealth is achievable for everyone on the planet but you know what stops the majority from getting it? Sacrifice!

If I told you that I could guarantee that your future descendants can live the most amazing life ever but there's just one catch, would you be intrigued? Most would be intrigued by such a proposition but of course their willingness to take the offer or walk away depends on that proverbial "catch." Here's the catch. In order for your grandchildren and all future descendants of yours to live the most amazing life ever, YOU have to live like crap for 10 year. I chose live like crap so they'll never have to

I know you're probably thinking, "what exactly do you mean...live like crap?" Almost anything on earth no matter how hard can be accomplished with intense focus for 10 years. When I say live like "crap" I mean a stripped down, bare bones minimum existence. Absolutely no extras, nothing above basic necessities. Things that you can actually live without, you go without them. No cable TV, no $5 lattes, no ball games, nothing but basic necessities for 10 years.

Most stand up guys are thinking, I can do that in a heart beat. Women for the most part have become accustomed to sacrificing for everyone else and are probably thinking this is nothing . Keep in mind though ladies, if you don't need it to live, you can't have it. No make up, no hair dresser, no perfumes and expensive body washes...just the bare necessities for 10 years. Men and women alike with any love for their children and future descendants will still likely agree that this is a fair exchange. You'll build generational wealth and your grandchildren and future descendants will live amazing lives because of your sacrifice and willingness to live like crap for the next 10 years. Here's where it gets interesting though. If at the time of this reading you don't have any children, you are truly in the best position to build generational wealth and leave a solid legacy using the plan that I'll outline below. However, if you already have children, this challenge just intensified 100X. If you're looking to build generational wealth and you already have children, then guess what. You have to convince them of the bare bones minimum lifestyle for 10 years too. No birthday parties, extra curricular activities at school, proms and homecomings don't exist, no Christmas, yep no Christmas at least not in the hyper commercialized way. Remember, this is a guarantee that their children will never know struggle and all of their descendants going forward will live the most amazing lives ever if they are willing to sacrifice for 10 years. Thing you can get the kiddos on board? Or is this the place where you check out and say things like, "money ain't everything," or "money can't buy happiness" or "the best things in life are free." Funny how we're quick to rationalize our current state when things get just a tab bit challenging.

Choose a shoestring budget before life chooses it for you.

10 Year Generational Wealth BluePrint

So...if you're still reading at this point you either don't have kids or you're intrigued enough to at least want to know what the plan is that you'll be convincing the children to buy into, right? Either way I'm glad you've decided to stick around. Just remember this blueprint is designed for an intense 10 year plan that will ensure that your grandchildren are wealthy, not You, not your children. However, I'll roll out an abbreviated plan that can get you there as well, cool?

"Why a bare bones minimum for 10 years?" you ask. It's simple, you have to understand the time interest on money. See, inflation cause money to lose value every single day. Therefore, in order to use money most effectively you have to exchange as much of it as possible and as often as possible for something that's going to at least retain it's value at the rate of inflation or grow in value at a pace faster than inflation. If inflation, historically, has increased at a rate of 2% annually and you're not getting a 2% increase on your job and your interest on your savings account is less than that, are you beginning to see why you're losing financially. Is it making sense to you why you have to do something as radical as a bare bones minimum lifestyle for 10 years. You need to take every single dollar you get above what it takes to live a bare bones minimum lifestyle and put it towards building generational wealth for the next 10 years. This will ensure that your grandchildren will inherit wealth and never have to worry about money. The 10 year generational wealth blueprint is simple, however we never confuse simple with easy. You're going to take every dime you get for the next 10 years and aim at 1 or 2 things, paying down debt or investing for double digit returns (see video below, most don't believe in getting double digit returns). That's it, that's the blueprint. If you do that for 10 straight years, no parties, no expensive dinners, no name brands, packed lunches for work, no upgrades in lifestyle whatsoever. A span of 10 year with this type of intense focus will change your life and your financial family tree forever. Numbers Never Lie

Disclaimer: This is NOT financial advise as I am not a licensed planner or advisor and NOT authorize to give financial advise. These examples are hypothetical and for information purposes only.

Now that we got that out the way let's look at some numbers. Say at the beginning of year 1 you literally cut all the fluff out of your life. No paid TV, gym membership gone, movie night cancelled, kids activities come to an end unless the can get sponsored, no more ripping and running burning valuable gas, all the things that we're "train" to do in a capitalistic society come to an end. For the average American household that would save a minimum of $500 per month. You save every single dime of the $500 for the first 6 months, now you have a $3,000 mini emergency fund established. Now that the mini emergency fund is established you spend the next 18 months attacking your debt with vengeance. You apply the $500 plus the original payment to the smallest balance owed and you do that until the balance is wiped out. The funny thing is, some of us have debts and the balance is less than $500 but instead of paying it off we pay the minimum and let the interest continue to compound. If the smallest balance had a $100 minimum payment, when you pay it off you've increased your monthly cash flow by $100. Now you have $600 to apply to the next lowest debt balance and you repeat the process until all of your debts are wiped out with the exception of your mortgage. Car notes, furniture, student loans, credit cards, cell phone leases, get rid of all of them. For the sake of time we're going to say you've done that and it took all of 3 years. Assuming that you have lost your job or lost any significant income, chances are you're $1500 - $2500 or more cash flow positive. Meaning the debt is gone but after you pay your mortgage and other residual bills, light, gas, water etc. you have money left over, that amount is your monthly cash flow. Save Your Money and Your Money Will Save You

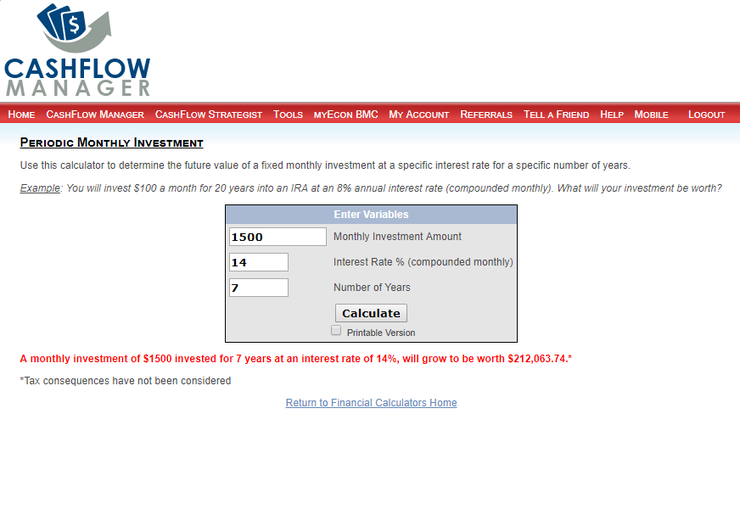

Let's be clear about one thing here. When I say "save your money" I'm not talking about putting it into a savings account. I'm talking about safe guarding it with your decisions and not letting it get away from you in a senseless fashion. If you make a habit of treating your money this way, it will in turn safe guard you as well. Now let's talk about what you can do with an extra $1500 per month for 7 years that will build generational wealth for you and your family.

The image above is a financial calculator called the CashFlow Manager in it I've plugged in your monthly cash flow of $1500 per month at 14% rate of return for 7 years, as it took 3 years to pay off debt and build the $1500 monthly cash flow. As you can see at a generous 14% your money would grow to $212,063.74. Now, let me reiterate, this plan is for generational wealth building, it's not for "YOU" to become wealthy it's for your grandchildren to inherit wealth. I can see you thinking that $212k is not a lot of wealth. Hang with me, let me show you how the grandbabies will inherit wealth then we'll talk about an accelerated plan for you to enjoy a little wealth.

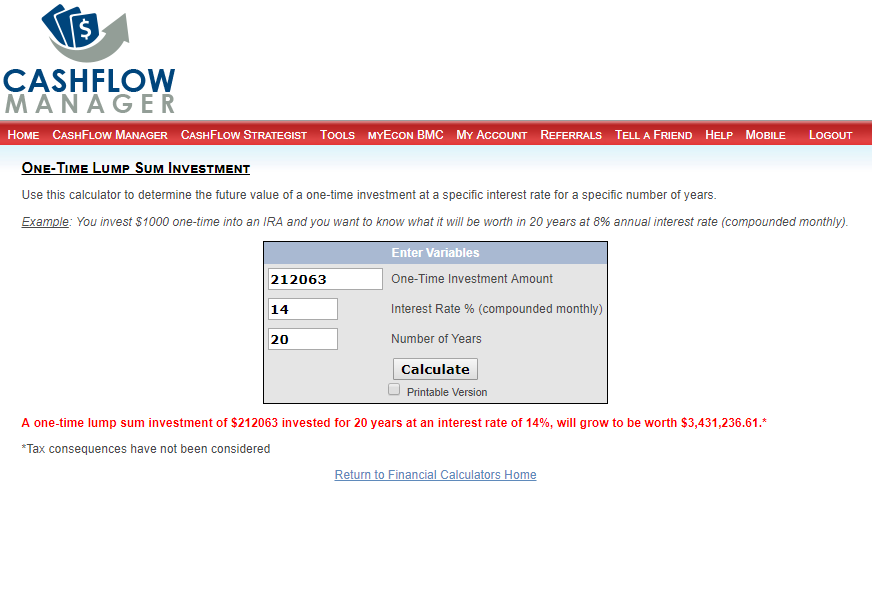

Lookie, lookie, lookie what 10 short years of sacrifice has produced. You basically lived like a hermit for 10 years so that your grandchildren can inherit $3,431,236.61. Do you think it'd be worth it. Can you do something this radical to end poverty in your bloodline forever? Because naturally you're going to be required to learn how this stuff works. This is just a silly example but as you're cutting back on your lifestyle, not going out as much, there's no cable TV so chances are you have a ton of free time. Might as well learn to invest, learn the real rules of capitalism. See I can say that you can end poverty in your bloodline forever because when you learn this stuff, you teach it to your children. When they inherit this wealth they have the financial I.Q. to manage it and make it grow.

Is it going to be easy, not at all. To pull something like this off, you have to fight like hell. Fight against those that don't understand and those that are satisfied with the status quo. You might have to fight with your mate as they might not be able to see the bigger picture. You're definitely going to have to fight with your children, at least early one, because they won't understand how saving $20 bucks on a movie ticket will radically change their future. But most of all you're going to have to fight with yourself. You have to fight to rise above average, you'll have to fight to stay disciplined and remain or course. It takes courage to build wealth. In the words of Damon Dash, "I hustle for my last name!" I encourage you to do the same. It's worth it and building generation is not only an option, it's our obligation! Wondering Where You Get Double Digit Returns? Check out this video and you'll see. This is how

|

AuthorH Cortez aka Financial Health Mentor to the Working Class Dave Ramsay CourseLife Insurance Quote/Review

Credit Restoration Made Easy

Buy Now!

Erase Debt for Good

Join My Team NOW!CashBack Shopping

Identity Protection

Affordable Roadside

Supplemental Insurance

Best Book for

|

Financial Health Mentor Generational Wealth Building Strategist

- Home

- Talking Money in the Morning LIVE!

- Black Wealth Movement

- Meet H Cortez

- Your Ad Here!

- Contact

- FHM Bookstore

- Black Wealth Survey

- BBC Generational Wealth Building Conference

- Black Wealth Survey Thank You

- Black Wealth Movement Intl

- Financial Freedom Fighters Giveaway

- Financial Freedom Fighters Giveaway Official Rules

RSS Feed

RSS Feed